U.S. Monetary Supply

The Concise Encyclopedia of Economics

Money Supply by Anna J. Schwartz, Economist at the

National Bureau of Economic Research, New York.

http://www.econlib.org/library/Enc/MoneySupply.html

What Is the Money Supply?

The U.S. money supply comprises currency—dollar bills

and coins issued by the Federal Reserve System and the U.S. Treasury—and

various kinds of deposits held by the public at commercial banks and other depository institutions such as thrifts and credit

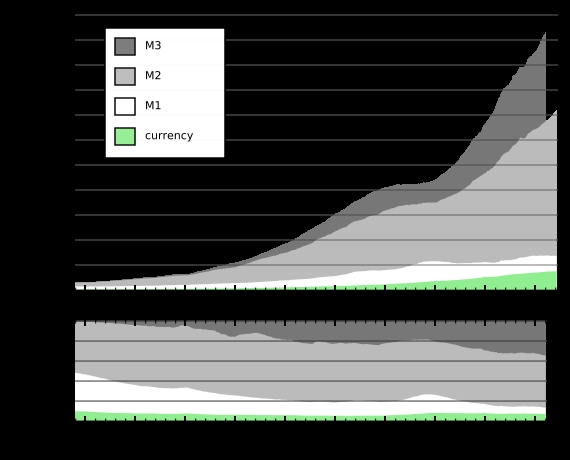

unions. On June 30, 2004, the money supply, measured as the sum of currency

and checking account deposits, totaled $1,333 billion. Including some types of savings deposits, the money supply totaled

$6,275 billion. An even broader measure totaled $9,275 billion.

These measures correspond to three definitions of money that

the Federal Reserve uses: M1, a narrow measure of money’s function as a

medium of exchange; M2, a broader measure that also reflects money’s function

as a store of value; and M3, a still broader measure that covers items that many

regard as close substitutes for money.

The definition of money has varied. For centuries, physical

commodities, most commonly silver or gold, served as money. Later, when paper money and checkable deposits were introduced,

they were convertible into commodity money. The abandonment of convertibility of money into a commodity since August 15, 1971,

when President Richard M. Nixon discontinued converting U.S. dollars into gold at $35 per ounce, has made the monies of the

United States and other countries into fiat money—money that national monetary authorities have the power to issue without

legal constraints.

What Determines the Money Supply?

Federal Reserve policy is the most important determinant

of the money supply. The Federal Reserve affects the money supply by affecting its most important component, bank deposits.

Here is how it works. The Federal Reserve requires depository

institutions (commercial banks and other financial institutions) to hold as reserves a fraction (typically 10%) of specified

deposit liabilities. Depository institutions hold these reserves as cash in their vaults or Automatic Teller Machines (ATMs)

and as deposits at Federal Reserve banks. In turn, the Federal Reserve controls reserves by lending money to depository institutions

and changing the Federal Reserve discount rate on these loans and by open-market operations. The Federal Reserve uses open-market

operations to either increase or decrease reserves. To increase reserves, the Federal Reserve buys U.S. Treasury securities

by writing a check drawn on itself. The seller of the treasury security deposits the check in a bank, increasing the seller’s

deposit. The bank, in turn, deposits the Federal Reserve check at its district Federal Reserve bank, thus increasing its reserves.

The opposite sequence occurs when the Federal Reserve sells treasury securities: the purchaser’s deposits fall, and,

in turn, the bank’s reserves fall.

If the Federal Reserve increases reserves, a single bank

can make loans up to the amount of its excess reserves, creating an equal amount of deposits. The banking system, however,

can create a multiple expansion of deposits. As each bank lends and creates a deposit, it loses reserves to other banks, which

use them to increase their loans and thus create new deposits, until all excess reserves are used up.

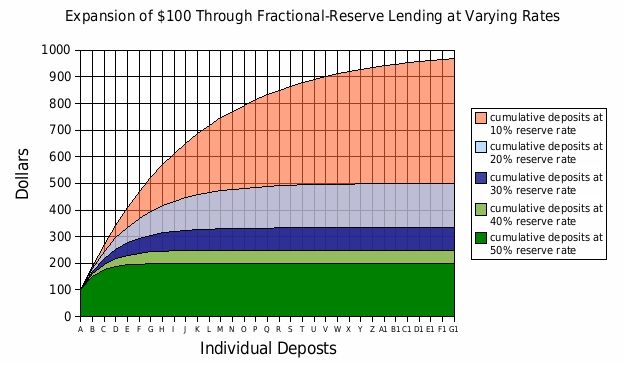

If the required reserve ratio is 10 percent, then starting

with new reserves of, say, $1,000, the most a bank can lend is $900, since it must keep $100 as reserves against the deposit

it simultaneously sets up. When the borrower writes a check against this amount in his bank A, the payee deposits it in his

bank B. Each new demand deposit that a bank receives creates an equal amount of new reserves. Bank B will now have additional

reserves of $900, of which it must keep $90 in reserves, so it can lend out only $810. The total of new loans the banking

system as a whole grants in this example will be ten times the initial amount of excess reserve, or $9,000: 900 + 810 + 729

+ 656.1 + 590.5, and so on. {Thus the Federal Reserve is printing money which is fed into our banking system and dispersal

through loans—consumer and commercial.[i]}

In a system with fractional reserve requirements, an increase

in bank reserves can support a multiple expansion of deposits, and a decrease can result in a multiple contraction of deposits.

The value of the multiplier depends on the required reserve ratio on deposits. A high required-reserve ratio lowers the value

of the multiplier. A low required-reserve ratio raises the value of the multiplier.

In 2004, banks with a total of $7 million in checkable deposits

were exempt from reserve requirements. Those with more than $7 million but less than $47.6 million in checkable deposits were

required to keep 3 percent of such accounts as reserves, while those with checkable accounts amounting to $47.6 million or

more were required to keep 10 percent. No reserves were required to be held against time deposits.

Even if there were no legal reserve requirements for banks,

they would still maintain required clearing balances as reserves with the Federal Reserve, whose ability to control the volume

of deposits would not be impaired. Banks would continue to keep reserves to enable them to clear debits arising from transactions

with other banks, to obtain currency to meet depositors’ demands, and to avoid a deficit as a result of imbalances in

clearings.

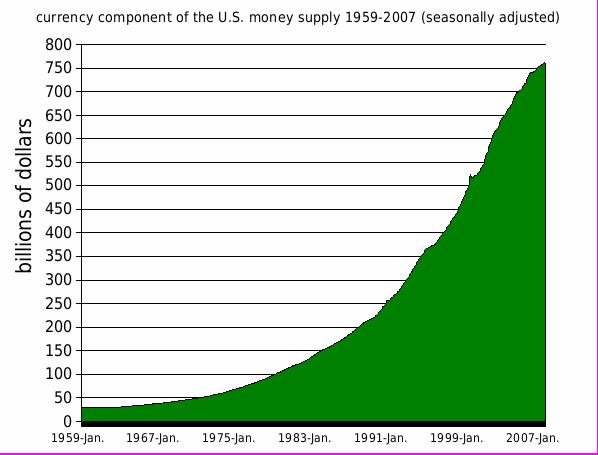

The currency component of the money supply, using the M2

definition of money, is far smaller than the deposit component. Currency includes both Federal Reserve notes and coins. The

Board of Governors places an order with the U.S. Bureau of Engraving and Printing for Federal Reserve notes for all the Reserve

Banks and then allocates the notes to each district Reserve Bank. Currently, the notes are no longer marked with the individual

district seal. The Federal Reserve Banks typically hold the notes in their vaults until sold at face value to commercial banks,

which pay private carriers to pick up the cash from their district Reserve Bank.

The Reserve Banks debit the commercial banks’ reserve

accounts as payment for the notes their customers demand. When the demand for notes falls, the Reserve Banks accept a return

flow of the notes from the commercial banks and credit their reserves.

The U.S.

mints design and manufacture U.S. coins for distribution to

Federal Reserve Banks. The Board of Governors places orders with the appropriate mints. The system buys coin at its face value

by crediting the U.S. Treasury’s account at the Reserve Banks. The Federal Reserve System holds its coins in 190 coin

terminals, which armored carrier companies own and operate. Commercial banks buy coins at face value from the Reserve Banks,

which receive payment by debiting the commercial banks’ reserve accounts. The commercial banks pay the full costs of

shipping the coin.

In a fractional reserve banking system, drains of currency

from banks reduce their reserves, and unless the Federal Reserve provides adequate additional amounts of currency and reserves,

a multiple contraction of deposits results, reducing the quantity of money. Currency and bank reserves added together equal

the monetary base, sometimes known as high-powered money. The Federal Reserve has the power to control the issue of both components.

By adjusting the levels of banks’ reserve balances, over several quarters it can achieve a desired rate of growth of

deposits and of the money supply. When the public and the banks change the ratio of their currency and reserves.

The

U.S. mints design and manufacture U.S.

coins for distribution to Federal Reserve Banks. The Board of Governors places orders with the appropriate mints. The system

buys coin at its face value by crediting the U.S. Treasury’s account at the Reserve Banks. The Federal Reserve System

holds its coins in 190 coin terminals, which armored carrier companies own and operate. Commercial banks buy coins at face

value from the Reserve Banks, which receive payment by debiting the commercial banks’ reserve accounts. The commercial

banks pay the full costs of shipping the coin.

In

a fractional reserve banking system, drains of currency from banks reduce their reserves, and unless the Federal Reserve provides

adequate additional amounts of currency and reserves, a multiple contraction of deposits results, reducing the quantity of

money. Currency and bank reserves added together equal the monetary base, sometimes known as high-powered money. The Federal

Reserve has the power to control the issue of both components. By adjusting the levels of banks’ reserve balances, over

several quarters it can achieve a desired rate of growth of deposits and of the money supply. When the public and the banks

change the ratio of their currency and reserves to deposits, the Federal Reserve can offset the effect on the money supply

by changing reserves and/or currency.

If

the Federal Reserve determines the magnitude of the money supply, what makes the nominal value of money in existence equal

to the amount people want to hold? A change in interest rates is one way to make that correspondence happen. A fall in interest

rates increases the amount of money people wish to hold, while a rise in interest rates decreases that amount. A change in

prices is another way to make the money supply equal the amount demanded. When people hold more nominal dollars than they

want, they spend them faster, causing prices to rise. These rising prices reduce the purchasing power of money until the amount

people want equals the amount available. Conversely, when people hold less money than they want, they spend more slowly, causing

prices to fall. As a result, the real value of money in existence just equals the amount people are willing to hold.

Changing

Federal Reserve Techniques

The

Federal Reserve’s techniques for achieving its desired level of reserves—both borrowed reserves that banks obtain

at the discount window and non-borrowed reserves that it provides by open-market purchases—have changed significantly

over time. At first, the Federal Reserve controlled the volume of reserves and of borrowing by member banks mainly by changing

the discount rate. It did so on the theory that borrowed reserves made member banks reluctant to extend loans because their

desire to repay their own indebtedness to the Federal Reserve as soon as possible was supposed to inhibit their willingness

to accommodate borrowers. In the 1920s, when the Federal Reserve discovered that open-market operations also created reserves,

changing nonborrowed reserves offered a more effective way to offset undesired changes in borrowing by member banks. In the

1950s, the Federal Reserve sought to control what are called free reserves, or excess reserves minus member bank borrowing.

The

Fed has interpreted a rise in interest rates as tighter monetary policy

and a fall as easier monetary policy. But interest rates are an imperfect indicator of monetary policy. If easy monetary policy

is expected to cause inflation, lenders demand a higher interest rate to compensate for this inflation, and borrowers are

willing to pay a higher rate because inflation reduces the value of the dollars they repay. Thus, an increase in expected

inflation increases interest rates. Between 1977 and 1979, for example, U.S.

monetary policy was easy and interest rates rose. Similarly, if tight monetary policy is expected to reduce inflation, interest

rates could fall.

From

1979 to 1982, when Paul Volcker was chairman of the Federal Reserve, the Fed tried to control non-borrowed reserves to achieve

its monetary target. The procedure produced large swings in both money growth and interest rates. Forcing non-borrowed reserves

to decline when above target led borrowed reserves to rise because the Federal Reserve allowed banks access to the discount

window when they sought this alternative source of reserves. Since then, the Federal Reserve has specified a narrow range

for the federal funds rate, the interest rate on overnight loans from one bank to another, as the instrument to achieve its

objectives. Although the Fed does not directly transact in the Fed funds market, when the Federal Reserve specifies a higher

Fed funds rate, it makes this higher rate stick by reducing the reserves it provides the entire financial system. When it

specifies a lower Fed funds rate, it makes this stick by providing increased reserves. The Fed funds market rate deviates

minimally from the target rate. If the deviation is greater, that is a signal to the Fed that the reserves it has provided

are not consistent with the funds rate it has announced. It will increase or reduce the reserves depending on the deviation.

The

big change in Federal Reserve objectives under Alan Greenspan’s chairmanship was the acknowledgment that its key responsibility

is to control inflation. The Federal Reserve adopted an implicit target for projected future inflation. Its success in meeting

its target has gained it credibility. The target has become the public’s expected inflation rate.[ii]

History of the U.S. Money Supply

From

the founding of the Federal Reserve in 1913 until the end of World War II, the money supply tended to grow at a higher rate

than the growth of nominal GNP. This increase in the ratio of money supply to GNP shows an increase in the amount of money

as a fraction of their income that people wanted to hold. From 1946 to 1980, nominal GNP tended to grow at a higher rate than

the growth of the money supply, an indication that the public reduced its money balances relative to income. Until 1986, money

balances grew relative to income; since then they have declined relative to income. Economists explain these movements by

changes in price expectations, as well as by changes in interest rates that make money holding more or less expensive. If

prices are expected to fall, the inducement to hold money balances rises since money will buy more if the expectations are

realized; similarly, if interest rates fall, the cost of holding money balances rather than spending or investing them declines.

If prices are expected to rise or interest rates rise, holding money rather than spending or investing it becomes more costly.

Since

1914 a sustained decline of the money supply has occurred during only three business cycle contractions, each of which was

severe as judged by the decline in output and rise in unemployment: 1920–1921,

1929–1933, and 1937–1938. The severity of the economic decline in each of these cyclical downturns, it is widely

accepted, was a consequence of the reduction in the quantity of money, particularly so for the downturn that began in 1929, when the quantity of money fell by an unprecedented one-third.

There have been no sustained declines in the quantity of money in the past six decades.

The

United States has experienced three major price inflations since 1914, and each has been

preceded and accompanied by a corresponding increase in the rate of growth of the money supply: 1914–1920, 1939–1948,

and 1967–1980. An acceleration of money growth in excess of real output growth has invariably produced inflation—in

these episodes and in many earlier examples in the United States and elsewhere

in the world.

Until

the Federal Reserve adopted an implicit inflation target in the 1990s, the money supply tended to rise more rapidly during

business cycle expansions than during business cycle contractions. The rate of rise tended to fall before the peak in business

and to increase before the trough. Prices rose during expansions and fell during contractions. This pattern is currently not

observed. Growth rates of money aggregates tend to be moderate and stable, although the Federal Reserve, like most central

banks, now ignores money aggregates in its framework and practice. A possibly unintended result of its success in controlling

inflation is that money aggregates have no predictive power with respect to prices.

The

lesson that the history of money supply teaches is that to ignore the magnitude of money supply changes is to court monetary

disorder. Time will tell whether the current monetary nirvana is enduring and a challenge to that lesson.

[ii] The problem is that through funny bookkeeping much that is inflation isn’t counted. For example, changes in the cost of food, energy, and most manufactured goods, among

other things are not used in determining the rate of inflation. The result of

this is benefits tied to the rate of inflation are reduced, including salaries, social security payments, and return on bank

deposits.